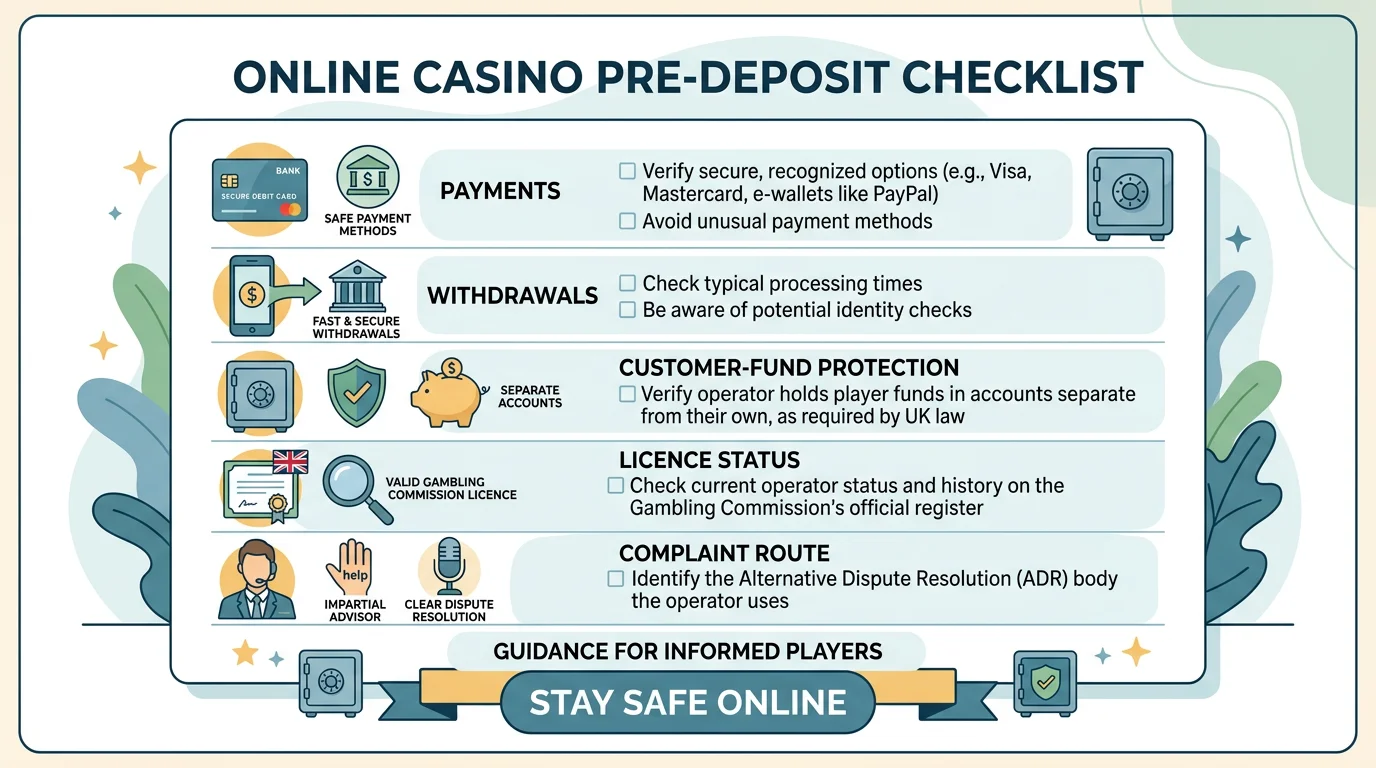

- Payments and withdrawal checks

- Data, privacy and marketing controls

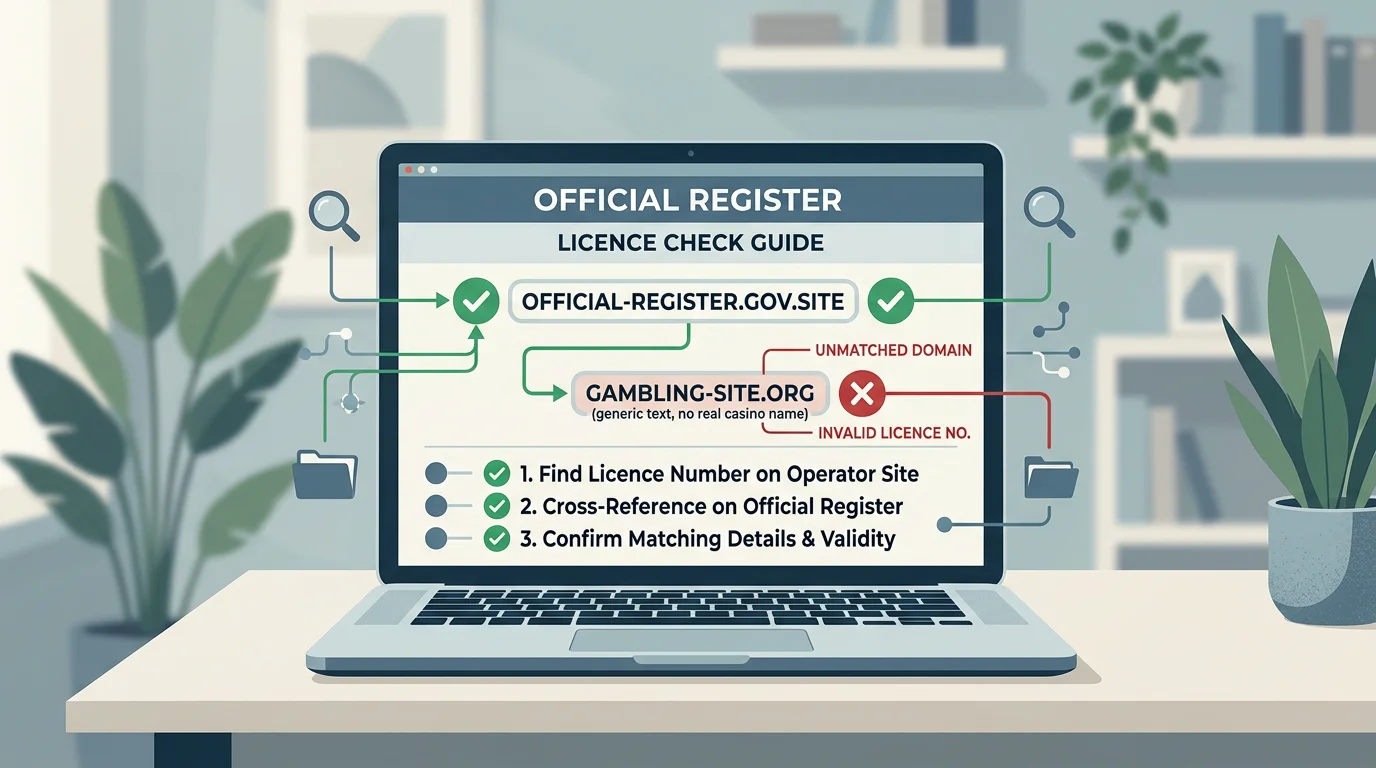

- Check the Gambling Commission register

- Self-exclusion and safer next steps

UK Casino ID Checks and Fast KYC Verification Rules

Table of Contents

- Identity Verification Checks for Fast Casino Withdrawals

- Withdrawal-stage checks need careful wording

- Different checks are not the same thing

- Financial vulnerability checks and risk-assessment wording

- Questions to ask before uploading documents

- Data concerns are valid, but they belong in the right place

- When checks trigger a gambling-control worry

Identity Verification Checks for Fast Casino Withdrawals

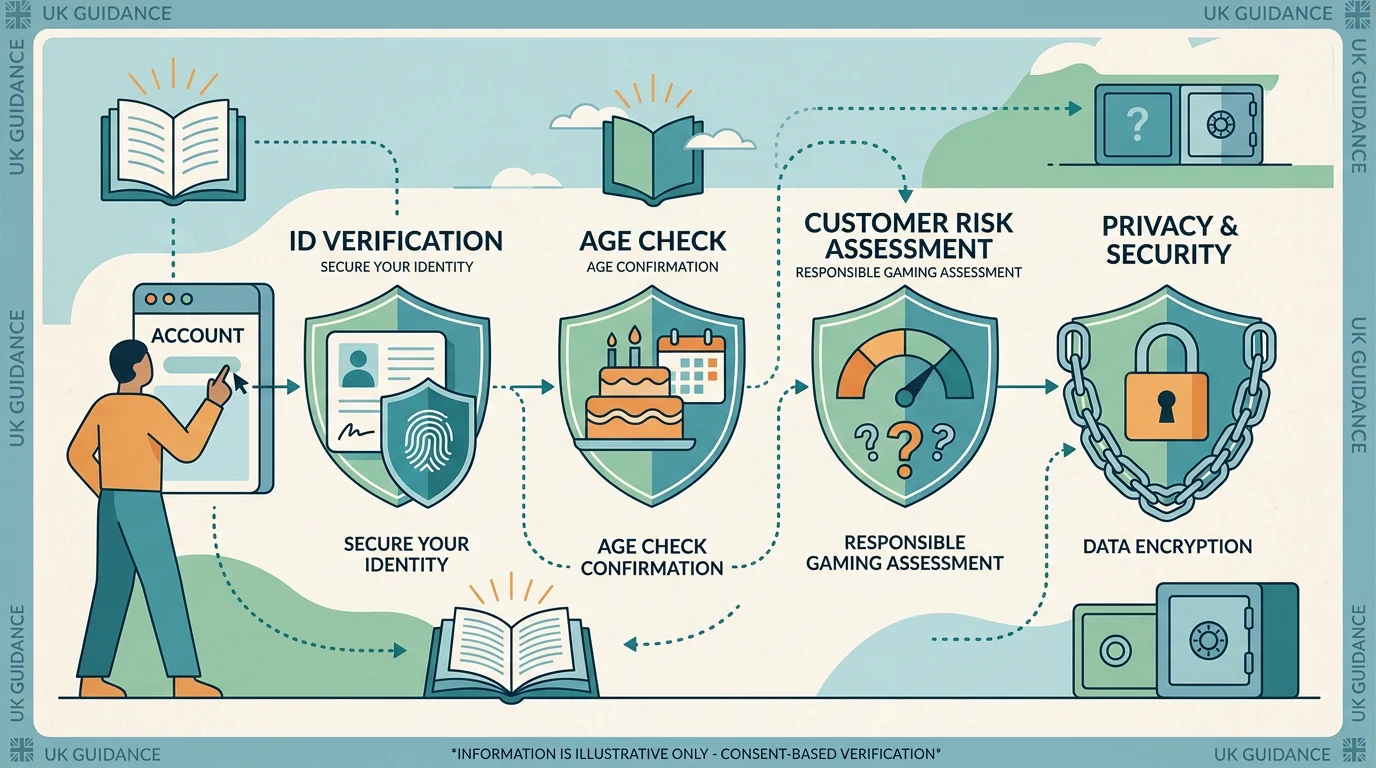

Online gambling businesses must verify age and identity before a person can gamble. The point is not only to stop underage gambling. Identity checks can also support self-exclusion, account security and legal checks. For someone looking at a site described as outside GAMSTOP, this matters because “easy sign-up” language may hide the more important question: who is checking that the account is lawful and protected?

Good verification wording should tell you what may be requested, why it may be requested, and when it may be requested. It should not ask you to ignore official checks or treat document review as an unfair obstacle. It is reasonable to want clear data handling and a fair process, but it is not safe to look for ways to avoid age, identity, anti-money-laundering or customer-risk controls.

A site that markets itself around avoiding ID checks may also be weak in other areas, such as licence clarity, withdrawal handling, customer support or safer gambling tools. That does not prove every outcome in advance, but it is enough reason to slow down. If the business is licensed for Great Britain, age and identity checks are not optional marketing extras.

Withdrawal-stage checks need careful wording

One common worry is being asked for documents when trying to withdraw. The Gambling Commission’s public guidance says a business cannot ask for age or identity proof as a condition of withdrawal if it could have asked for that proof earlier. That is an important boundary, but it should not be turned into a promise that no withdrawal-stage questions can ever arise.

There may still be legal reasons for information at withdrawal, including checks connected with anti-money-laundering duties or other account-risk concerns. The practical lesson is to read the verification section before depositing. Do not wait until there is money in the account to find out what the business says it may ask for, what documents it accepts, and how it explains delays.

If a withdrawal is delayed, avoid making new deposits while trying to force a different result. Keep records, read the complaint route, and separate the document question from bonus, payment and balance questions. If the problem is about customer funds or payment timing, use the payments and withdrawals guide. If it becomes a formal complaint, use the dispute route rather than relying on pressure or repeated chat messages.

Different checks are not the same thing

| Check type | Plain meaning | What to ask before you play |

|---|---|---|

| Age verification | Confirmation that the customer is old enough to gamble. | Does the site explain that age is checked before gambling? |

| Identity verification | Confirmation that the account holder is who they say they are. | What documents or electronic checks may be used, and when? |

| Legal and customer-risk information | Information used for duties such as anti-money-laundering controls, self-exclusion checks or account security. | Does the business explain why extra information may be requested? |

| Financial vulnerability checks | For remote licensees, checks linked to public-record indicators when net deposits pass the stated threshold. | Does the account information explain how customer risk is handled in clear, non-alarming language? |

| Financial risk assessments | The Gambling Commission update of 16 April 2026 said these were not live and were not affordability checks. | Is the wording current, specific and consistent with official public information? |

Financial vulnerability checks and risk-assessment wording

Financial wording can be confusing because several terms sound similar. One verified rule for remote licensees is the financial vulnerability check condition. From 28 February 2025, the condition sets checks at deposits minus withdrawals exceeding £150 in a rolling 30-day period and uses public-record indicators such as bankruptcy and certain debt judgments or orders. That is specific wording, not a general licence for anyone to demand unlimited information for any reason.

Financial risk assessments are a separate topic. In the Gambling Commission update of 16 April 2026, financial risk assessments were described as not live and not affordability checks. That matters because public discussion often mixes these phrases together. When reading account terms, look for exact wording rather than broad statements such as “we may run affordability checks” without explanation.

Even where a check is legitimate, the explanation should be clear. You can ask whether the term says what triggers the check, what kind of information is used, how the account may be affected, and where to complain if the explanation is unclear. Those are fair questions. They are not a method for avoiding checks.

Questions to ask before uploading documents

- Is the gambling business shown on the official register, and do the name and domain match?

- Does the site explain why documents may be requested before gambling, at account review, or at withdrawal?

- Does the privacy information explain how personal data and documents are handled?

- Does the account page separate age, identity, legal, security and financial wording?

- Is the complaint route visible if a document request or delay is unclear?

- Does the site imply that avoiding checks is a selling point?

If the answer to the last question is yes, treat that as a warning sign. A no-check promise can be attractive when you want speed, privacy or a quick withdrawal, but it may also mean fewer protections and a harder route if something goes wrong.

A common red flag involves predatory terms, so always review the payments, withdrawals and customer-fund checks carefully.

Data concerns are valid, but they belong in the right place

Worrying about personal data is reasonable. Identity documents, address information and financial-risk wording are sensitive. The answer is not to use a site that avoids verification. The answer is to check who the business is, read the privacy information, understand what data may be requested, and avoid sending documents to a business whose licence and domain information do not make sense.

This page explains why checks happen and how to read them. It does not give legal advice about a document dispute or tell you which documents to provide. For data rights, marketing preferences and account-security questions, read the data and marketing guide. For licence status, start with the register-check guide.

When checks trigger a gambling-control worry

Sometimes the strongest reaction to verification is not about privacy. It is about being blocked from gambling when the urge to continue is high. If you are looking for a way around checks, self-exclusion, bank blocks or account limits, pause and treat that as a protection signal. The safer next step is support, not another account.

Use the self-exclusion and support guide for practical next steps. If money pressure is involved, do not treat document approval as the thing that will fix the situation. A verified account can still lead to losses, and an unverified or weakly checked site can create additional problems with withdrawals, data and complaints.

Protecting your money is the primary goal of our independent Great Britain casino guide.

Creado por la redacción de «Casino not on Gamstop».